Guyana’s offshore oil fields produced a quarter billion barrels of crude in 2025, supported by a steep fourth-quarter ramp-up that widened the set of markets taking its oil.

Actual production data released by the Guyana government for the first 10 months shows accumulated output of more than 206 million barrels, while export data indicates continued strong production in the last two months, pushing the total output for the year to the quarter-billion mark.

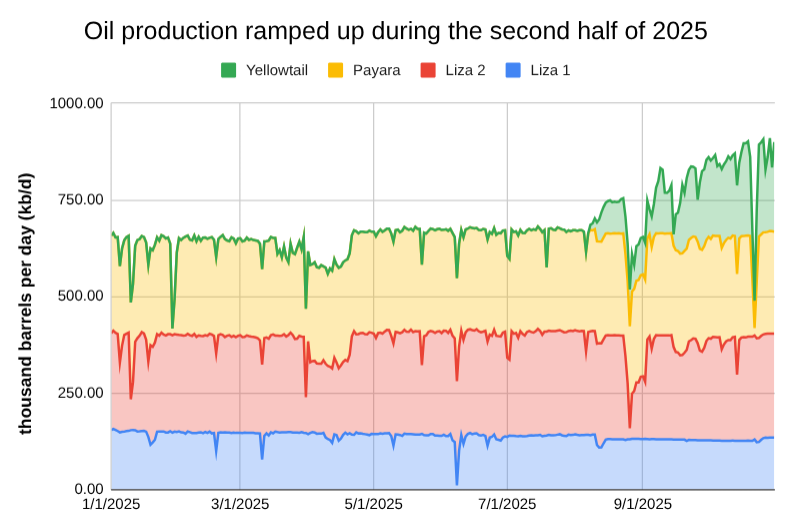

The sharpest gains came in the fourth quarter. Three projects in operation for most of the year — Liza Phase 1, Liza Phase 2, and Payara — lifted their production; a fourth, Yellowtail, came online in August and reached its nameplate capacity of 250,000 barrels per day (bpd) in early November.

Average national output for the year stood above 700,000 bpd, with the highest rates recorded in the final quarter. Liza Phase 1 averaged more than 130,000 bpd, Liza Phase 2 more than 240,000 bpd, Payara more than 250,000 bpd, and Yellowtail more than 160,000 bpd over its first five months.

The expansion continues a trend that began when Guyana started producing oil in December 2019. Output increases each year as new projects start up and the company debottlenecks existing facilities beyond initial design rates. ExxonMobil Guyana will pursue debottlenecking at Yellowtail, potentially boosting its capacity beyond 250,000 bpd.

This rapid growth has triggered significant spillover effects across the economy, supporting several years of double-digit economic expansion and driving investment in construction, manufacturing, and services.

Guyana exports all of the crude produced offshore. Under a Production Sharing Agreement, the government receives its contractual share, which it then markets through contracted traders. Private partners lift the remainder.

Shipping data tracked throughout the year shows that Europe remained the dominant regional buyer of Guyana’s crude. The Netherlands and Panama were the most common direct destinations, mainly as transshipment hubs that route cargoes onward to other markets.

Other regular destinations included the United States, the United Kingdom, Italy, Germany, Spain, Brazil, Poland, and the Bahamas. Less common but regular buyers included Turkey, China, and India.

Market dynamics shifted throughout the year as European refiners faced an oversupply of sweet crude. Rising production offshore Guyana added to the available supply, pushing prices lower and making the barrels more competitive for refiners in distant markets.

As a result, more cargoes from Guyana reached Asian countries towards the end of the year, including China, India, Malaysia, and Thailand. A combination of lower prices, an increase in available barrels, and a growing number of refiners willing to try Guyana’s crude has expanded the market footprint. Experts anticipate that this trend will continue through 2026.

A fifth development, with a capacity of 250,000 bpd, is scheduled to come online and will lift national production beyond the one-million-bpd mark. Even in a lower-price environment, Guyana’s crude is gaining a foothold among a growing list of refiners because of its broader market reach.

{kind=link}